Can you believe it’s already the end of the year?

Here are five stories that will help you look ahead to 2022:

- Mortgage ‘loyalty tax’ rises

- Property listings trending up

- Average loan size jumps 16.4%

- Govt boosts first home buyer support

- Broker market share hits new record

Read more below.

|

|

|

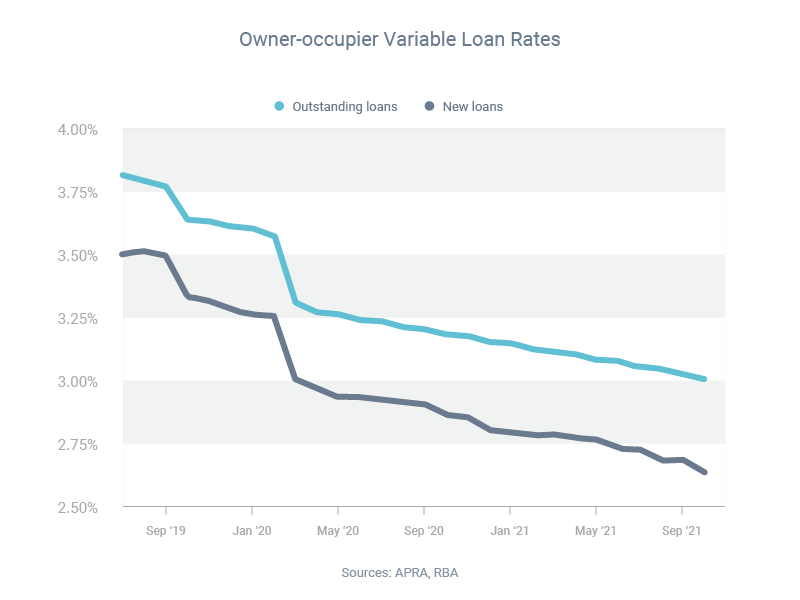

You might not realise that lenders often charge lower interest rates to new borrowers compared to existing customers.

Over the past year, as the graph from the Reserve Bank of Australia shows, this gap has widened.

|

|

|

Back in October 2020, owner-occupiers who took out new variable loans were charged, on average, 0.32 percentage points less than existing borrowers. By October 2021, this gap had grown to 0.37 percentage points.

If the RBA increases the cash rate next year, as many economists predict, it will be interesting to see if this gap widens or narrows as lenders bid to undercut their rivals and grab more market share.

|

|

|

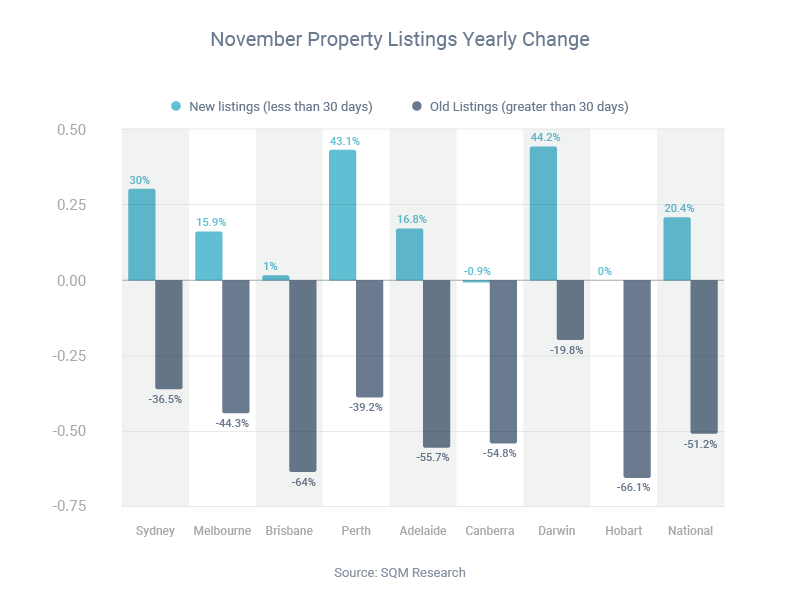

More property listings are coming onto the market, which should give buyers more choice in 2022.

In November, another 96,346 properties were listed for sale, according to SQM Research. This was 2.3% higher than the month before and 20.4% higher than the year before.

As the charts show, while there’s been a significant increase in new listings, there’s been a big decrease in old listings. That suggests many of these homes have finally found buyers.

|

|

|

If buyers have more properties to choose from in 2022, it’s likely homes will take longer to sell.

Properties listed on realestate.com.au during November took an average of 30 days to sell, which is incredibly low by historical standards. The year before, the figure was 44 days.

In November, the amount of new listings added to realestate.com.au reached their “highest level in a decade” for capital cities and “highest level in five years” for regional locations.

|

|

|

An extra 4,651 first home buyers will be able to access federal government assistance during the 2021-22 financial year.

The government had originally pledged to support 20,000 first home buyers this year – 10,000 under the First Home Loan Deposit Scheme and 10,000 under the New Home Guarantee.

Now, the government has added an extra 4,651 places, which went unused during the 2020-21 financial year.

The First Home Loan Deposit Scheme lets eligible first home buyers purchase a home with just a 5% deposit, without having to pay lender’s mortgage insurance. The New Home Guarantee is almost identical, except it applies to new builds, off-the-plan properties and house-and-land packages. The government hasn’t stipulated where the extra 4,651 places will be allocated, but it seems likely they will be spread over both programs, based on demand.

|

|

|

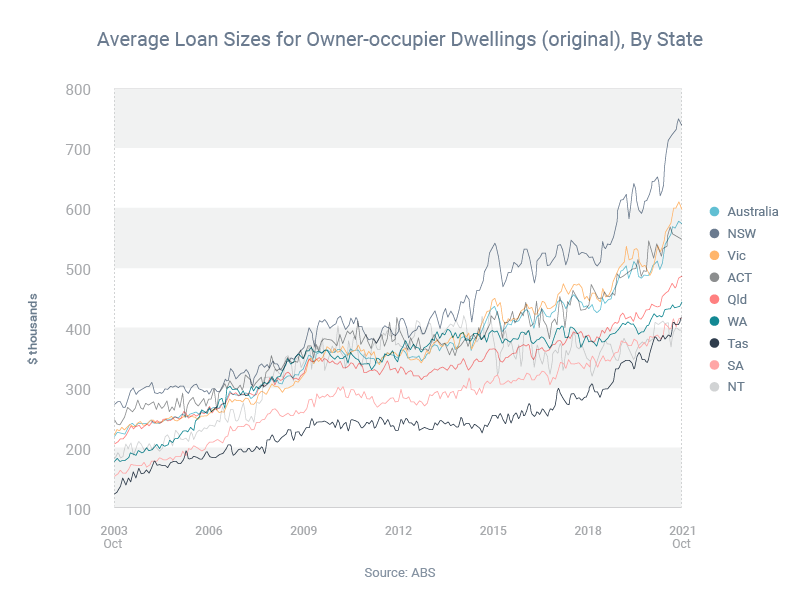

Over the year to October, the size of the average Australian home loan increased 16.4%, according to the latest data from the Australian Bureau of Statistics.

Loan sizes also increased in every individual state and territory, as the graph shows.

|

|

|

Naturally, the amount of money you borrow is very important. But so is the share of money you borrow compared to the value of the property you purchase.

This is known as your loan-to-value ratio (LVR). For example, if you borrowed $800,000 to buy a $1 million property, your LVR would be 80%.

The lower your LVR, the more likely lenders will offer you lower interest rates and special deals. Conversely, if your LVR is above 80%, you will probably have to pay lender’s mortgage insurance (LMI), an insurance policy to protect the lender in case the borrower defaults.

If you’re planning to buy in 2022, it’s important you think about:

- What your LVR is likely to be

- Whether you can aim for a lower LVR to access lower interest rates

- Whether you’re willing to pay LMI to enter the market early

The key is to be prepared and to crunch the numbers. I can help you with both tasks.

|

|

|

In the September quarter, mortgage brokers originated a record 66.9% of all new residential home loans, according to research group Comparator.

This compares to market share of 60.1% the year before.

Why is broker market share growing so strongly?

One reason is value. When you go directly to a bank, you will only get told about that bank’s products. But when you go to a mortgage broker, the broker will compare loans from a wide variety of lenders.

Another reason is ethics. Brokers have to follow the Best Interests Duty, which legally obliges them to work in their clients’ best interests. Banks, though, are not bound by the Best Interests Duty. Broker market share is likely to keep increasing, due to the rollout of open banking, a system that makes it easy for consumers to share their data with third parties. Brokers will be able to use open banking to help clients shop around and find more suitable loans.

|

|

|

Thanks for your support this year. If there’s anything I can do to help you and your family in 2022, please let me know.

Kind Regards,

Declan Hanratty

0409 089 456

|

|

|

3/178b Gooch Street

THORNBURY VIC 3071

|

Australian Credit Licence No. 383120

383120

|

|

|

ActivePipe Message ID: 866843