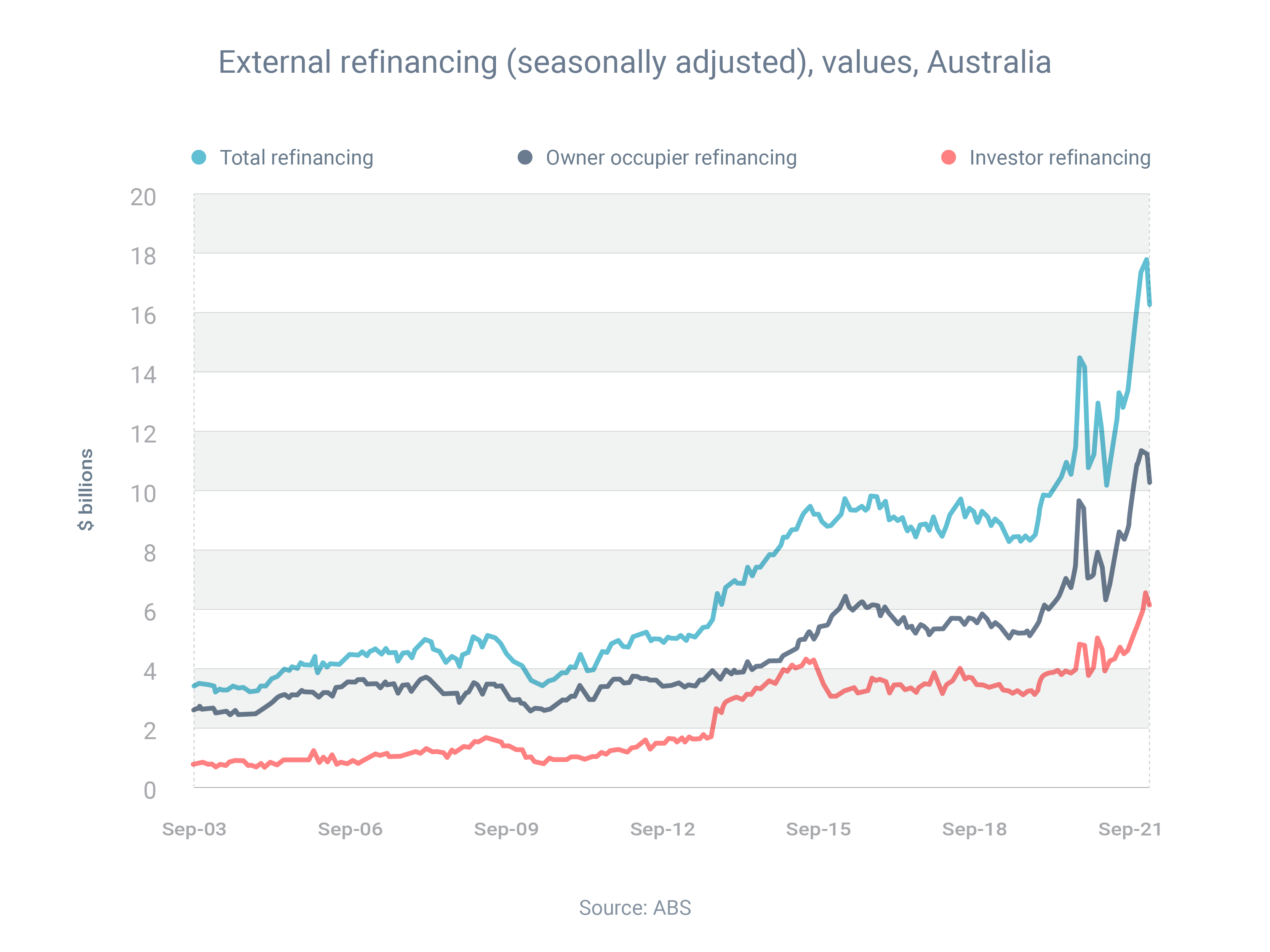

In recent weeks, a host of lenders, including all of the big four banks, have increased their fixed rates, which might be causing some more borrowers to consider refinancing.

Also, some people might be thinking about refinancing to take advantage of equity they’ve built up in their home during the ongoing property boom.

So if you’re thinking about refinancing, you’re not alone. That said, you should refinance when it makes sense for your personal situation, not because other people are doing so or because the media is speculating about interest rate movements.

Depending on your scenario, refinancing might allow you to:

- Reduce your interest rate

- Switch your interest rate type (i.e. variable to fixed)

- Pull out equity to fund the deposit on an investment property

- Consolidate several higher-rate debts into a new lower-rate home loan

- Get a loan with better features

Want to know if refinancing is right for you? I’ll be happy to talk you through the pros and cons.